Greater Pasadena Market November 5 — Locked-In Sellers, Savvy Buyers & Rising ARMs.

The Greater Pasadena Market November 5 shows a market in motion—but not in the ways many expect. Prices remain steady, buyers are getting creative, and the invisible hand holding back supply isn’t rates—it’s taxes. Meanwhile, ARMs are back on the scene as affordability tightens.

1 | Local Market Snapshot.

Pasadena: Median $1.20 M, 37 DOM, 95 sales (+19 % YoY). Homes under $1.5 M move fastest when turnkey.

South Pasadena: $1.50 M (–4.8 % YoY), 42 DOM; buyers more selective.

Altadena: ≈ $1.10 M (–16 % YoY); negotiation power returning.

La Cañada Flintridge: ≈ $2.2 M (+16 % YoY), 31 DOM; updated homes still compete fiercely.

Across the Greater Pasadena Market November 5, inventory remains roughly 20–25 % below pre-pandemic averages, keeping leverage with sellers of move-in-ready homes.

2 | The “Stay-Put Penalty” Explained.

Since 1997, homeowners have been allowed to exclude $250 K (single) or $500 K (joint) of capital gains on a home sale. Those limits were never indexed to inflation.

Example: A couple who bought in 1998 for $400 K and now could sell for $1.6 M would face ≈ $700 K in taxable gain. That tax shock keeps many in place, shrinking inventory—the classic “stay-put penalty.”

Prop 19 lets Californians 55 + carry property-tax bases, but it doesn’t touch capital-gains tax exposure.

The proposed More Homes on the Market Act would double those exclusions and index them to inflation, potentially freeing millions of homes nationwide.

Locally, that matters: the Greater Pasadena Market November 5 depends heavily on long-held properties. Until reform passes, low turnover will remain a defining constraint.

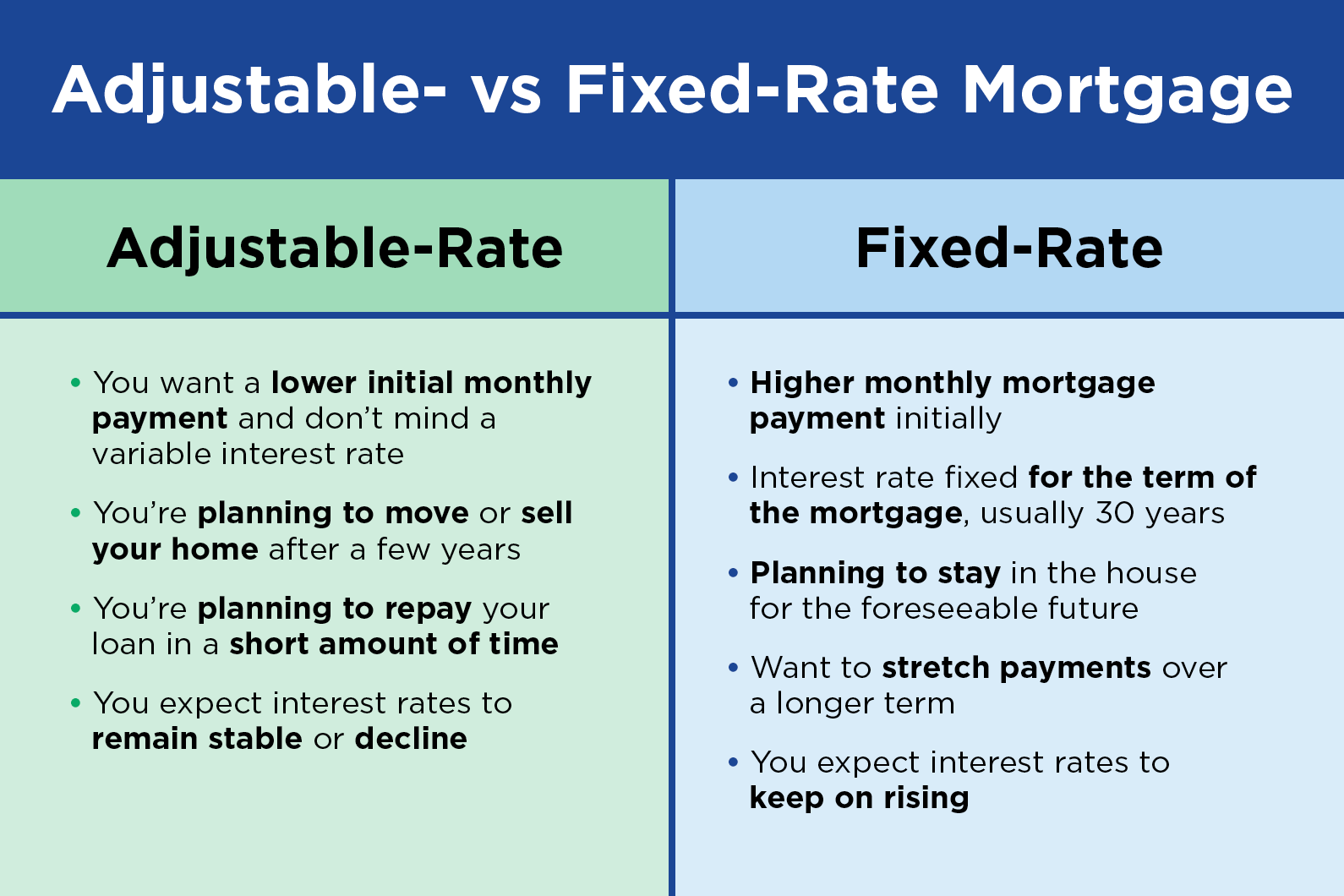

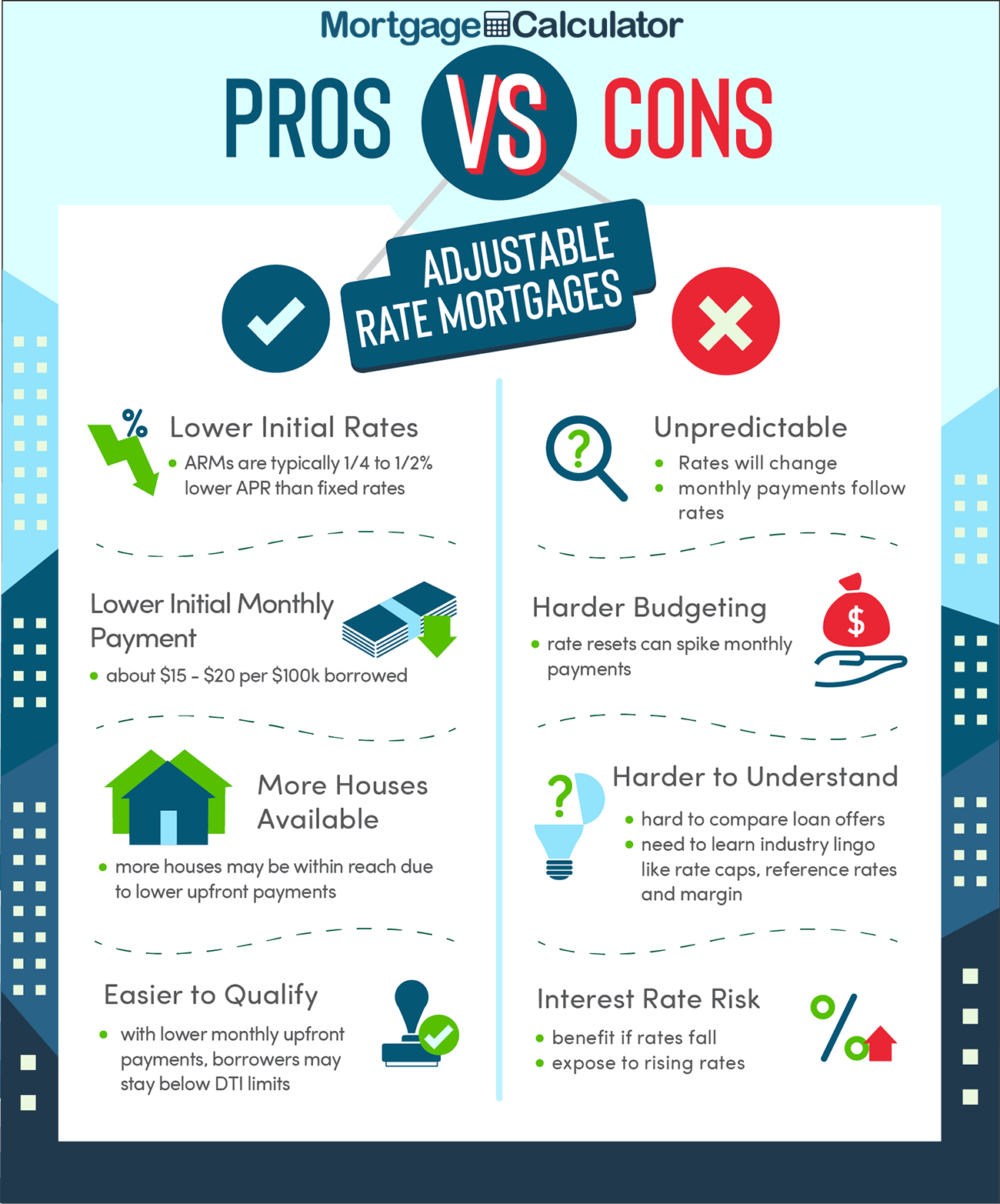

3 | New Buyer Behavior — ARMs Return.

With 30-year fixed rates hovering near 6.5 %, more buyers are eyeing adjustable-rate mortgages for relief. Nationally, ARMs now represent ≈ 9.6 % of all new loan applications, the highest share since late 2023. (HousingWire, Oct 2025).

In Greater Pasadena, especially Pasadena and La Cañada, buyers using 5/6- or 7/6-year ARMs can cut their initial rate by roughly 0.75–1 point—hundreds per month in savings.

Caution: If rates rise or the home isn’t refinanced before adjustment, payments can jump. But for clients planning a 5–7 year hold, the math can work.

The Greater Pasadena Market November 5 sees this as a tactical play, not speculation—buyers managing cost while staying flexible.

4 | Macro Context.

The delayed CPI (+0.31 % MoM, +3 % YoY) shows inflation cooling. Jobless claims edged up, and insurance premiums keep rising—1 in 5 owners say they’re under-insured. The Fed’s next move is likely a 25-bp cut, but data gaps from the shutdown make timing uncertain.

All told, the macro backdrop continues to support a cautious but active Greater Pasadena Market November 5.

5 | Strategy Moves.

Buyers:

- Explore ARMs or hybrid loans if you expect a 5–7 year hold.

- Target 30-day+ listings for leverage; keep appraisal contingencies tight.

- Model insurance and maintenance in affordability.

Sellers:

- Price for today’s comps, not last spring’s.

- Highlight condition + energy / insurance resilience.

- Consult your CPA about capital-gain exposure before listing.

- Use Hem-young’s micro-market snapshot to see what’s truly selling near you.

6 | What Could Shift Next.

- Congressional movement on the More Homes on the Market Act → inventory unlock.

- Sustained ARM growth → fresh buyer energy in higher price bands.

- Further Fed cuts → Q1 2026 bounce for entry-level homes.

The Greater Pasadena Market November 5 remains steady but selective—an environment that rewards preparation and precision.

Hem-young’s Closing Insight.

“Market averages don’t sell homes—micro-markets do. Two blocks can tell two different stories,” notes Hem-young de Fazio, Compass REALTOR®.

Request your personalized micro-market snapshot to see what’s happening on your street.